Salman Ahmed Shaikh

In many countries, there is a situation of lockdown for quite some time. It is uncertain how much time will it take to get back business as usual and life as normal. Businesses are struggling with the closure of markets, production facilities and sales outlets. Even e-commerce has taken a hit due to restrictions on commute and transportation.

In economics, we recognize four factors of production, i.e. land, labour, capital and entrepreneurship. As an entrepreneur, one has to bear the business risk. After paying all factor payments from the sales revenue, the net return of productive enterprise could turn out to be positive or negative.

During the lockdown period following the outbreak of COVID-19 globally, many business owners would be forced to absorb losses after paying factor payments. When the businesses do not have enough work, they could lay off employees. Thus, people providing labour services would also suffer by losing employment or having to remain in employment without salaries. People who had provided land on rent for commercial use usually get rent no matter whether the business makes a profit or loss and no matter whether the land is used or remain idle. However, the tenant can at least evacuate the property taken on rent and come out of the contract.

In contrast, the capital provider does not undertake such risks. The lender provides capital at some predetermined interest rate. The interest will accrue with time and it has no connection with how much the capital earns from the investment in the business. The borrower cannot avoid interest payment. It cannot even repay the principal before the maturity without incurring additional penalties in most cases. If the payment is delayed, the interest will accrue on the outstanding interest liability from the previous period. The interest payment liability will increase at an exponential rate if not paid on time. Let us try to understand it from the example of Corona Virus. If the virus had been growing at a linear rate, it would not have been that much dangerous. It is the exponential increase in the Corona Virus spread which makes it become uncontrollable and create havoc in the society. Compound interest in the financial system is such a Corona Virus. Interest accrued but unpaid increases interest in the future periods ahead at an exponential rate.

On the other hand, Islamic banking has some distinct economic differences over the interest-based financial intermediation. Islamic banking as a form of financial intermediation offers potential in reinforcing links between finance and the real economy.

Islamic banks can only earn income from the trade of assets or by providing the usufruct of real assets. This ensures that their profits are linked with real assets in the economy. They cannot simply lend money and earn compound interest on it.

One can examine Islamic modes of financing and say that clients taking Islamic leasing and financing products also have to return their due obligations related to the assets in the form of rents and price of assets on time. However, there are some differences which become more apparent in the times of crisis.

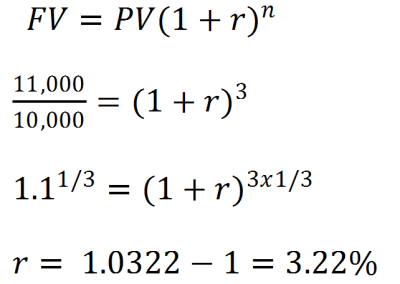

For instance, consider a corporate customer who purchases a real asset on Murabaha financing basis at $11,000. The spot price of the asset on cash payment is $9,000. Islamic bank purchases the asset in the spot market and pays the price. Islamic bank takes the ownership and constructive possession of the asset. Until the asset is sold to the client, Islamic bank bears the risks related to the real assets. In order to bring efficiency, transparency and cost competitiveness, Islamic bank engages customer as agent to purchase the real asset on bank’s behalf and take constructive possession of the asset. In order to reduce its own risk, Islamic bank takes insurance cover for the asset. Islamic bank would charge a price that will enable it to earn profits after deducting all direct and indirect costs which arise in the form of price of asset, insurance, installation, transportation and taxes, for instance. Let us suppose that the insurance, installation, transportation, taxes, duties and documentation related costs sum up to $1,000. Thus, the total investment by the bank is $10,000 (Present Value or PV).

If the transaction goes as per plan, Islamic bank would earn a profit of $1,000, which is a 10% return on its invested funds. If the customer delays payment for 3 years or 5 years, then the Islamic bank can only charge price of $11,000. In case, the payment of $11,000 (Future Value or FV) is received after 3 years, the return on investment ‘r’ would turn out to be 3.22% as illustrated below.

In case, the payment of $11,000 (Future Value or FV) is received after 5 years, the return on investment ‘r’ would turn out to be 1.92% as illustrated below.

On the other hand, the conventional bank would earn compounded interest on delayed payment at the prevailing interest rate. Islamic bank would receive the Murabaha price of $11,000 no matter whether the price is received after 1 year, 2 years, 3 years, 4 years or 5 years. In contrast, the conventional bank would charge interest on its outstanding loan amount as long as the payment is not made. If the prevailing interest rate is 10%, the conventional bank would get $11,000 if payment is received after 1 year. If payment is delayed, then the conventional bank will get $12,100, $13,310, $14,641 and $16,105 if payment is received after 2, 3, 4 or 5 years respectively.

One can still argue that Islamic banks also charge penalties on late payment. To maintain financial discipline, it is important to have a deterrent against wilful and unjustified delays in payment. In practice, the customer is asked to sign a unilateral undertaking in which the customer unilaterally promises to pay to charity an amount of money if the customer delays payments without any justifiable reason. Nonetheless, this promise remains unilateral and the Islamic bank does not take the charity amount received from the customer as its income. The reason why Islamic bank is allowed to receive and administer the charity amount on late payment is that it will ensure that the client pays to charity and does not avoid it. Hence, this payment to charity serves as a deterrent to discourage late payment, but it is not meant to compensate the bank. Having such a deterrent would encourage timely payments and which will protect the depositors from losing their investments. Thus, Islamic debt based modes of financing have some distinctions over the conventional finance.

Islamic equity based modes of financing are even more distinct and egalitarian. Musharakah in Islamic finance refers to a joint enterprise in which all the partners share the profit or loss of the joint venture. Mudarabah in Islamic finance refers to a joint enterprise in which one partner provides capital and another partner provides skills and effort. Profit is shared based on the pre-agreed profit sharing ratio. On the other hand, the loss is shared as per the capital contribution ratio.

The contract of Musharakah is imbued with the spirit of risk sharing rather than risk shifting or risk avoidance. No partner has a fixed share in profit unlike the case in lending on interest where the lender gets a stipulated return on the amount lent irrespective of whether the borrower earns profit or loss from that loan. Thus, from the viewpoint of distributive justice and income distribution, Musharakah is one of the ideal modes of financing to achieve inclusivity, economic mobility and equitable distribution of income. On the other hand, Mudarabah is even more effective to achieve inclusivity, economic mobility and equitable distribution of income by providing finance to a completely capital-deficient, but skilful person. In Mudarabah, the investing partner does not have a fixed share in profit unlike the case in lending on interest where the lender gets a stipulated return on the amount lent irrespective of whether the borrower earns profit or loss from that loan.

Categories: Articles on Islamic Finance

Great article Dr. Sahab. Mashallah

LikeLike