Salman Ahmed Shaikh

In medium to long term fixed finance, either Ijarah or Diminishing Musharakah is utilized in Islamic banking. The bank aims to cover the cost of fixed assets and earn some profit. The client wants asset acquisition with an ability to use the asset without having to pay the total cost upfront and yet be able to acquire the asset in due course of time.

Since banks want to recoup investment in fixed assets along with profit, they divide their investment in assets in number of units which usually equal the total months in the financing arrangement in Diminishing Musharakah. They can use the same mechanism to be able to recoup investment in fixed assets.

However, in determining profits, they can use rental index instead of interbank interest based benchmarks. This will make the Islamic lease transaction detached from interest-based benchmarks genuinely. In lease based contracts, such as Ijarah and Diminishing Musharakah, the rental indices can capture the true essence of pricing as per the nature of transaction.

Table below compares the two possible pricing structures in Islamic lease contracts in house finance.

| Risk/Payoff | Covering Principal Investment | Covering Profits |

| Low to Moderate Risk | Asset value divided in units and investment recovered when customer purchases units at historical price. | Rents are based on rental indices computed as an average of rental yields in a jurisdiction. |

| Moderate to High Risk | Asset value divided in units and investment recovered when customer purchases units at market price. Secondary market trade data will be used to determine market price. | Rents are based on rental indices computed as an average of rental yields in a jurisdiction. |

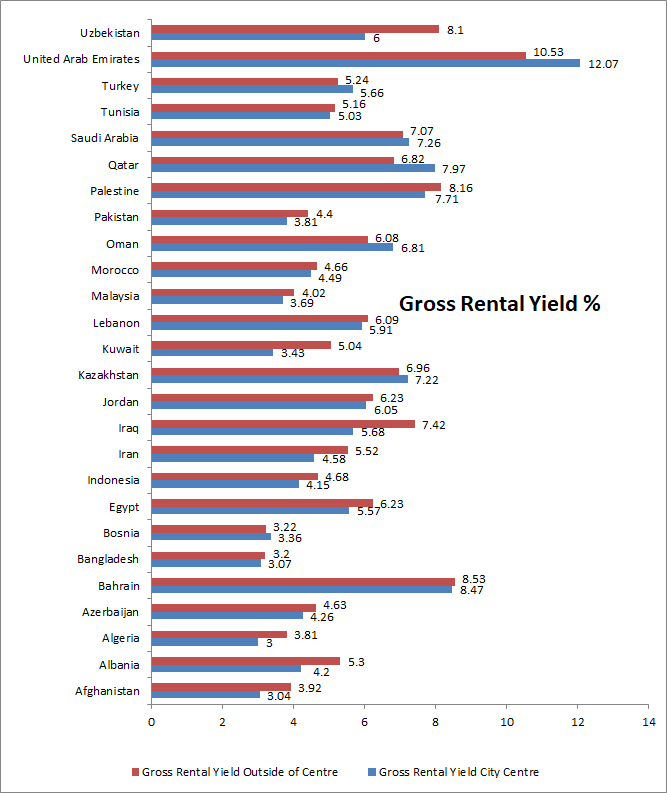

In real estate, rental yields vary from 3% per annum to 6% in most of the Muslim majority countries as can be seen in the graph below which takes data for 2020 from Numbeo.

These rental yields are stable and can provide a stable base rate over which risk premium and amortization rate can be added. Since the actual rental yields as base rates are very stable, there is expected to be greater acceptability given the low, but stable and expectedly positive rental yield plus the allowance to add risk, term and amortization factor in pricing.

In home financing, a similar rental index can be used through transaction based data available from the rental platforms, such as Zillow, Mudah, Realtors and Zameen, for instance. If the electronic platforms which facilitate renting and trade of real estate are used with appropriate randomization of sampled data, control and filter, then the updated data can be obtained for short term as well.

Rental yields or prices as reported in trading platforms represent market view and such cannot be manipulated if sufficient and random sample data is taken with appropriate control and filters.

Such rental indices can be developed in a different way as well by each country’s Bureau of Statistics. After all, they take such data into account indirectly for developing price indices as well as in measuring household living standards.

Table below proposes a possible pricing structure in Islamic lease contracts in car finance.

| Risk/Payoff | Covering Principal Investment | Covering Profits |

| Low to Moderate Risk | Car value divided in potential productive KMs during the life and investment is recovered when customer pays periodic rent. | Trade in secondary market at a lower value of i) Exercise price (keeping target profit in view) or ii) Market price so that bank achieves target return without increasing commercial displacement risk. |

In car finance, a renal index can be developed using the fare structure of ride hailing services, such as Uber, Lyft, Grab and Careem.

Rental index will be based on inputs like i) useful life of vehicle in kilometres, ii) tenure of financing, and iii) per kilometre fare in Uber/Careem/Lyft/Grab based on car type or on per KM saving in travelling distance. The monthly rent to cover asset cost can be derived as:

Monthly Rent = (Useful Life in KM / Tenor) x Per KM Fare

The car price could be fixed with a target profit in mind or it could be market based. In the latter case, residual value can be derived from sufficient number of transactions via AutoTrader, CarsDirect and Pakwheels, for instance.

Numerical Illustration of Car Ijarah with Profit on Resale

| Particulars | Amount (Rs.) |

| Vehicle Price at Spot | 2,000,000 |

| Useful Life in KM | 200,000 |

| Per KM Charge | 10 |

| Category | C |

| Total Lease Months | 60 |

| Monthly Rent (Rs.) | 33,333 |

| Total Rent (Rs.) | 2,000,000 |

| Resale After Lease Maturity at Market Price (Rs.) | 500,000 |

| Total Bank Profit = Rent +Resale Value – Purchase Cost | 500,000 |

The table below compares the potential strengths of this proposal along with possible challenges in its implementation.

Pros and Cons of Rental Indices

| Potential Strengths of the Option | Possible Challenges |

| Asset specific pricing benchmark reflecting relevant risks. | Rental indices may have more fluctuations, less widely available for sub-urban/rural regions and expose the banks to asset price risk. |

| With rise in asset pricing, bank has a potential to profit from asset price appreciation. | There is no term premium. It will have to be added separately. |

| Avoids reference to interest based benchmarks. | With escalating asset pricing, currency depreciation, inflation and other factors, asset prices and rents may go up and affect the consumers’ cost adversely causing commercial displacement risk. |

Categories: Articles on Islamic Finance