Salman Ahmed Shaikh

Regulators have been urging market participants to replace Interbank Offered Rates (IBOR) with recommended Risk Free Rates (RFRs) which tend to be backward-looking overnight reference rates – in contrast to IBORs which are forward-looking. Table 1 presents the list of key RFRs that will replace the LIBOR in different countries.

With LIBOR, the rate is fixed at the start of the relevant transaction period, and therefore a borrower will know what the mark-up amount will be for that period. With RFRs, the rate is measured on each day over the transaction period, and therefore the total financing cost payable will only be known at the end of the transaction period. Risk Free Rates are backward-looking overnight rates that, if applied to a calculation period, can only be determined at the end of that period. Table 1 lists some of the alternate reference rates.

Table 1: Alternative Reference Rates

| Currency | Current | Alternate Reference rate | Transaction Type | Administrator |

| USD | USD LIBOR | Secured Overnight Financing Rate (SOFR) | Secured | Federal Reserve Bank of NY |

| GBP | GBP LIBOR | Sterling Overnight Index Average (SONIA) | Unsecured | Bank of England (BoE) |

| EUR | EURIBOR | European Short Term Euro Rate (ESTER) | Unsecured | European Central Bank (ECB) |

| YEN | JPY LIBOR | Tokyo Overnight Average Rate (TONAR) | Unsecured | Bank of Japan (BoJ) |

| CHF | CHF LIBOR | Swiss Average Rate Overnight (SARON) | Secured | SIX Swiss Exchange |

On the other hand, RFRs are considered to be more robust as they are based upon a larger volume of observable transactions. Table 2 gives the comparison between IBOR and ARR or RFR.

Table 2: Difference between Alternate Reference Rates and Interbank Offered Rates

| Alternate Reference Rates | Interbank Offered Rate |

| Risk-Free. No maturity and credit risk premium | Includes the risk level of banks |

| Overnight | Available for tenors from overnight to 12 months |

| Transaction-based | Based on subjective submissions by banks |

| Backward looking | Forward looking |

| Require spread adjustment for maturity and risk premium | Only require adjustment beyond bank credit risk since that is already incorporated. |

| ARR + Credit Adjustment Spread + Margin | LIBOR + Margin |

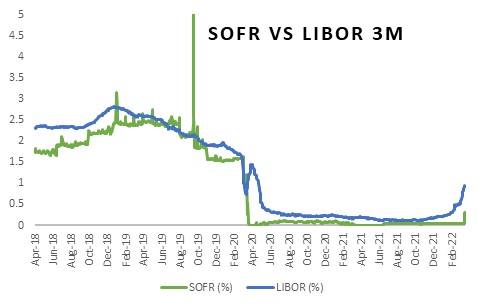

Figure below illustrates the movement of SOFR and USD 3-month LIBOR. Both have moved in tandem mostly. Since 3-month LIBOR is unsecured and has term premium, the curve of 3-month LIBOR is slightly above SOFR in most periods. In terms of volatility, SOFR has a standard deviation of 1.030 while USD 3-month LIBOR has a standard deviation of 1.048 during the period starting from Apr-2018 and ending at Mar-22. In terms of providing a robust measure which is based on actual and voluminous transactions, SOFR is much ahead in terms of LIBOR since LIBOR after the great financial crisis of 2007-09 became more and more opaque and less transparent. On average, the daily trading volume of transactions in SOFR is nearly $1 trillion.

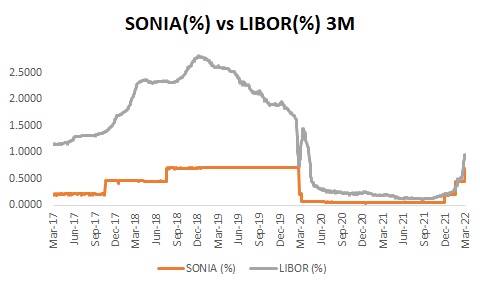

Furthermore, Figure below illustrates the movement of SONIA and USD 3-month LIBOR. Comparing Sterling Overnight Index Average (SONIA) with USD 3-month LIBOR, the relative stability of SONIA vis-à-vis USD 3-month LIBOR is quite visibly evident. During the period starting from Mar-2017 and ending at Mar-2022, the standard deviation of SONIA had remained at 0.2777 as against the standard deviation of USD 3-month LIBOR, which remained at 0.9468.

From the Islamic finance industry perspective, an important criterion for the industry wide adoption of any benchmark, particularly one that is published every business day, is the simplicity, reliability and robustness of its methodology.

Additionally, to engender the confidence of financial market participants, an interbank benchmark must be calculated frequently enough with a transparent and simple methodology open to public scrutiny.

In Islamic finance, an additional and most important aspect is Shari’ah compliance of the method as well as the instrument which is used in pricing.

In this regard, a key challenge is that are there currently a sufficient volume of underlying transactions on which an international Islamic interbank rate could be built? What would be the agreed methodology and basis of calculation? Who would be responsible for determining such rate? Would that rate be sufficiently robust?

Some additional challenges in transitioning to a different benchmark in Islamic finance include the following.

- Commercial Displacement Risk: Since Islamic banks genuinely strive to pass through actual returns to investing depositors, any significant change in cash flows will affect profit distribution and may lead to loss of competitiveness. Paradox is that similarity in cash is beneficial from the perspective of risk, especially commercial displacement risk. However, it increases the reputation risk since people evaluating Islamic banking and conventional banking on cash flow terms find no major signs of difference in cash flows.

- More Fluctuations, Volatility and Uncertainty: In the absence of low interbank market activity in Islamic finance space, if a real economy based benchmark is used, it will expose Islamic banks to newer and different risks in the macro economy. Thus, there is increased risk of volatility.

- Arbitrage Opportunity: If same benchmark is not used across financing types, then there is possibility of arbitrage opportunities by swapping assets.

- Yield Curve: If there are different benchmarks for different financing types, then it is difficult to find a well behaved yield curve and hence asset liability management will become a challenge.

- Frictions in Borrowing: There is flexibility in providing finance, but not when one needs finance since the industry in most countries is dominated by interest-based banking. Therefore, the stakeholders do not just include Islamic banks and Islamic financial institutions. Rather, it is also important that any new alternative is also acceptable to the counterparties including both Islamic and conventional financial institutions in the financial market.

- Willingness and Capacity of Stakeholders: Absorption capacity and willingness is required both from the bank as well as customers. Banks may be inclined to take on more risk, but the risk averse depositors may not prefer that. Bank as a delegated monitor of depositors is not using its own investment. Rather, it is an agent for the depositors to monitor the financing portfolio on investors behalf.

- Dual Objective Problem: Pricing alternate is desired to be distinctive yet closely follow the market dynamics. Both objectives may not be complementary and compatible with each other.

- Need for Multi-Functional Alternative: Sovereign rates or policy rates are primary pricing tools which affect interbank transactions as well. Policy rate not only serves as a pricing benchmark in financing transactions in interbank market, but also allows the central banks to effectively implement monetary policy by affecting money supply, controlling inflation, liquidity and hence aggregate demand. Changes in aggregate demand affect output growth and employment.

- Predictability of Pricing Alternative: Data for most real economic indicators from macroeconomics perspective is based on historical information. Such indicators should be forecastable to serve in determining forward looking expected profit rate.

Categories: Articles on Islamic Finance