Salman Ahmed Shaikh

As LIBOR has been phased out at the end of 2021, financial markets are switching towards Alternate Reference Rates (ARRs). These are also known as Risk Free Rates (RFRs). For instance, in North America, Secured Overnight Reference Rates (SOFR) is an overnight reference rate that broadly measures the cost of borrowing cash with U.S. Treasuries as collateral.

Repo transactions are not compliant with Islamic principles due to the buyback nature of transaction plus the use of interest based securities as underlying assets. However, in commercial contracts where Islamic banks would like to earn return, there is need for a pricing benchmark to mitigate risk as well as ensure transparency in the contract.

One alternative measure is seasonally adjusted output price index that measures core inflation (non-food, non-energy) after appropriate smoothing through linear, non-linear or exponential moving averages. If costs remain same in a short period of time, increase in output price positively influences profitability and such average price changes may truly reflect profitability in the real sector of the economy. CPI excludes cost of debt and tracks only price of assets, commodities and real services.

Price indices are available on weekly basis. For particular asset class and commodities, such indices can be developed on daily basis as well.

For consumer and corporate finance, Consumer Price Index (CPI) or Wholesale Price Index (WPI) can be used. In commodity based trade finance contracts, commodity price indices can be used. According to mainstream Islamic scholarship, inflation or gold indexation is not allowed in loans. But, if Murabaha is used instead of Qard, it is allowed to have difference in spot and deferred price provided it is not changed later on.

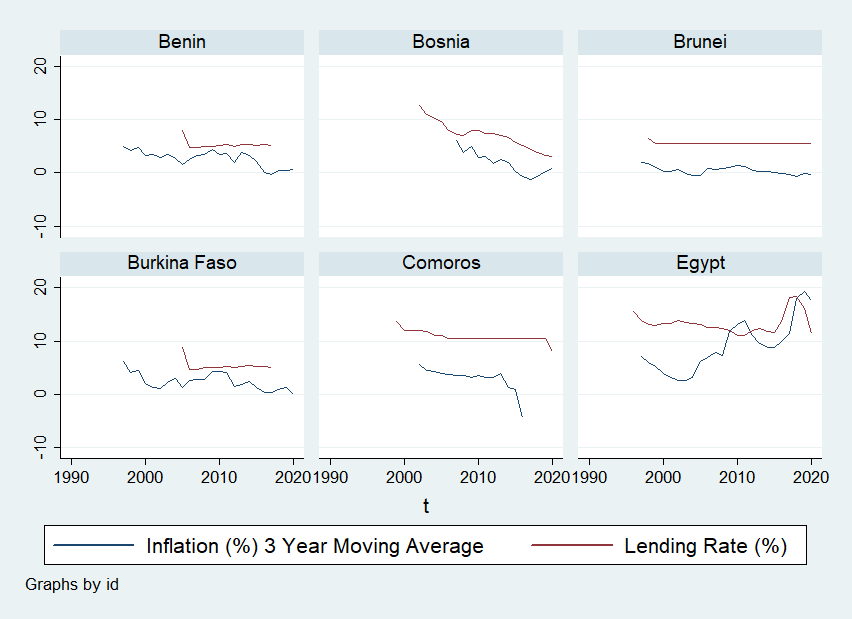

If inflation rate series is made smoother through moving average, then both the interbank rate and inflation rate are expected to covary. We know from macroeconomic theory that real interest rate is affected by inflation. There can be lead-lag bi-directional relationship theoretically. But, on average, in the long run, both are expected to co-vary.

If output price index (without taking percentage change for computing inflation) is plotted against time, it generally increases with time. Thus, an index based on output price of real assets and services can capture time value of economic resources. From the perspective of purchasing power differences, inflation as discount rate is a better indicator to be used in capital budgeting, security analysis, and discounted cash flow models.

However, decision would be required to choose among numerous output price indices with difference in weights, composition of basket of commodities, base year, frequency of publishing, audience (wholesale, retail), calculations (chain-weighted; fixed weighted) and formula (Laspeyres, Paasche, Fisher). A question naturally arises is that is there a precedent to use output price growth as a benchmark in some instruments and contracts in the financial world. The answer is that there are examples of inflation-linked bonds and Treasury Inflation Protected Securities (TIPS). However, they are not many and do not have the comparable volumes of trade as in RFRs based repo transactions. Table below summarizes the strengths and challenges of this alternative as a pricing benchmark.

| Potential Strengths | Possible Challenges |

| Frequency of data availability is weekly and instantaneous for commodities as compared to other real economy measures. | For banks, credit or deferred price is more relevant rather than spot price. Term premium will need to be added separately. |

| Banks can potentially gain from asset price appreciation and can preemptively invest in commodities in jurisdictions where it is allowed. Seasonal adjustment can make price fluctuations smoother. | Numerous output price index with difference in weights, composition of basket of commodities, base year, frequency of publishing, audience (wholesale, retail), calculations (chain-weighted; fixed weighted) and formula (Laspeyres, Paasche, Fisher) |

| Avoids reference to interest based benchmarks. Inflation statistics are measured by Bureau of Statistics and the Calculating Agent in this case does not have any conflicts-of interest. | Bank is exposed to asset price risk and supply side factors of the real economy. |

Figures below illustrate the time series relationship between 3 year moving average of inflation rate and weighted average lending rate. Inflation as measured by the percentage change in consumer price index reflects the annual percentage change in the cost to the average consumer of acquiring a basket of goods and services that may be fixed or changed at specified intervals, such as yearly. The Laspeyres formula is generally used. On the other hand, lending rate is the bank rate that usually meets the short- and medium-term financing needs of the private sector.

The data is obtained from World Bank for the 25 year period from 1996 to 2020 for 39 Muslim majority countries. The graphs of each country provide a preliminary illustration of co-movement of both inflation rate and lending rate when the former is smoothed using moving averages.

Thus, this proposal can be further explored by the Islamic financial institutions and regulators. This indicator is already widely available and analysts at central bank, financial institutions and financial markets closely watch and forecast this variable.

Central banks in many countries employ inflation targeting regime in monetary management. The frequency of publishing of this data is weekly even without changing current infrastructure.

If more resources are allocated by the Calculating Agent, then this can be a viable alternate benchmark for Islamic financial institutions given that it is a real economy based indicator and reflects higher profitability prospects with rise in output prices, keeping other things constant.

Finally, in most countries in most periods, the moving average of inflation rate moves below the lending rate. Thus, as a benchmark, it does not fall in the problem of starting with a very high base rate. Since credit risk premium and maturity premium are to be added further, it is handy to have a benchmark which is stable and yet starts with a relatively low base rate. Comments and feedback are welcome. Contact for more extensive data analysis at: islamiceconomicsproject@gmail.com

Categories: Articles on Islamic Finance